Arab Canada News – News for the Arab Community in Canada

News

Bank of Canada faces its last decision this year amid confusing data… and fears of monetary policy tightening in 2026

Strong economy and "stubborn" inflation: intertwined data shaping the Bank of Canada's decision and 2026 forecasts

Published: December 8, 2025

Bank of Canada is preparing this week to issue its final decision on the interest rate for 2025, at a time when conflicting indicators about the Canadian economy’s situation in 2026 are increasing, between a relatively strong labor market, inflationary pressures that have not completely eased, and ongoing repercussions of the trade war with the United States.

Despite this complex scene, the majority of economists agree that the bank will keep the key interest rate steady at 2.25%, a level that policymakers have reiterated in previous meetings as appropriate to achieve the 2% inflation target while allowing the economy to continue adapting to the “structural transformation phase.”

Meanwhile, the US Federal Reserve is preparing on the same day for a new quarter-point interest rate cut, to settle in a range between 3.75% and 4.00%, highlighting a difference in the pace of monetary policy between Ottawa and Washington.

Surprising job growth changes the economic picture

Since the bank’s October meeting, Canada has witnessed a series of economic data that surprised analysts and prompted some to reconsider how much the economy needs further monetary easing:

The economy added about 54,000 jobs in November, after strong gains also in September and October.

The unemployment rate dropped from 6.9% to 6.5%, marking the second consecutive monthly decline.

Wage growth remained steady, and total hours worked in the economy increased.

Revisions to GDP and productivity data showed that the economy’s performance over the past months was better than initial estimates reflected.

Economic growth in the third quarter reached 2.6% year-on-year, while the Bank of Canada had expected weak growth of only 0.5%.

These figures, according to analysts at major banks, mean that the Canadian economy has surpassed the phase of severe weakness caused by US tariffs mid-year, although the effects of the trade dispute remain on specific sectors.

Inflation eases… but not enough to reassure the bank

On prices, overall inflation rates have declined from the peak of recent years, but core inflation measures—which the bank relies on to judge medium-term trends—are still above comfortable levels.

Recent economic reports indicate that:

Some core inflation indicators remained above 2% in October.

Ongoing wage settlements, inventory costs, and supply chain restructuring continue to pressure prices.

The services sector, including rents and some household and personal services, still contributes to keeping inflation at a relatively “warm” level.

Therefore, analysts expect the Bank of Canada to reaffirm in its statement that the current interest rate is the “appropriate level at present” to keep inflation close to the target, while simultaneously emphasizing the bank’s readiness to move up or down if inflation and growth expectations change substantially.

Uneven recovery… and ongoing trade concerns

Despite improvements in the labor market and overall growth figures, experts warn that the recovery is uneven across sectors and regions:

Some export-related industries still suffer from uncertainty due to US tariffs on Canadian goods.

The manufacturing sector is cautiously responding to challenges related to supply chains and external demand.

Domestic consumption has begun to show signs of improvement but remains affected by high living costs in housing and food.

Economists at major commercial banks point out that the central bank’s “reserve margins” have become narrower, as it cannot cut rates much in an unstable inflationary environment, nor raise them quickly for fear of stifling the emerging recovery.

Why does this week’s decision seem relatively “decided”?

Based on most forecasts:

There are no immediate signals requiring an immediate rate hike, with inflation remaining on a gradual downward trend.

At the same time, strong employment and improved growth make it difficult to justify a new rate cut at this stage.

Therefore, analysts expect the bank to adopt cautious language, such as:

Affirming that the interest rate is at the “almost right level”

Indicating close monitoring of inflation trends, especially in the first half of 2026

Avoiding explicit signals about the timing of any future rate hikes or cuts

In other words, the bank’s expected message: “wait and assess” rather than quick action.

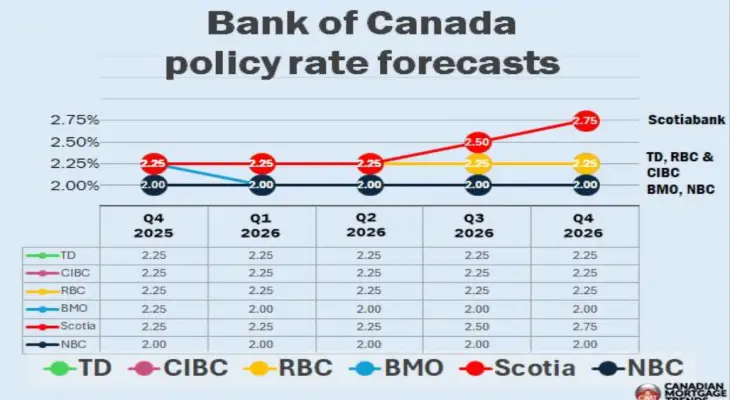

The discussion moves to 2026: Is it time to consider raising rates?

While this week’s meeting outcome seems almost decided, the discussion among economists and investors focuses on the 2026 path.

Financial markets have started pricing in the possibility of a rate hike in late 2026, with improving employment and growth data.

Some models used by bank analysts (such as “Taylor rule” scenarios) indicate that the current interest rate may be about 25–50 basis points below the theoretically appropriate level to contain inflationary pressures.

Other estimates talk about the possibility of a gradual increase totaling 50 basis points starting in the third quarter of 2026, if the economy continues to improve and price pressures remain above target.

On the other hand, some warn against excessive optimism:

The trade dispute with the United States remains a risk to exports and investment.

Any new shock to supply chains or energy prices could push inflation back up.

High levels of Canadian household debt may make them more sensitive to any sharp and rapid rate hikes.

What does this mean for consumers and the mortgage market?

For Canadian households and mortgage holders:

Keeping rates steady now means a continued period of relative stability in borrowing costs in the short term.

However, increasing talk about possible future rate hikes prompts experts to advise borrowers to be mindful of their ability to withstand a scenario of about half a percentage point or more rate increase in 2026.

The housing market may temporarily benefit from a stable interest rate environment, but any shift toward monetary tightening could later pressure prices and debt affordability.

This week: a steady and expected decision to keep rates at 2.25%, with a cautious and wait-and-see tone.

In 2026:

An increasing likelihood of a complete stop to the rate-cutting cycle

And the start of a serious discussion about raising rates if the economy continues to improve and core inflation remains above target.

In other words, Bank of Canada is not rushing to change course now, but it sends—through data and discussions around 2026—a clear signal that the “era of forever low rates is over,” and that the Canadian economy is entering a more delicate phase requiring a sensitive balance between supporting growth and curbing inflation.

Wednesday, 03 June 2026

Loading...

--°C

--°C

- --%

- -- kmh

- --%